Yun Jessica Meng, Licensed Immigration Adviser at IMME Limited, discusses how LIAs and Financial Advisers can cooperate effectively in terms of Migrant Investor Category.

Yun Jessica Meng, Licensed Immigration Adviser at IMME Limited, discusses how LIAs and Financial Advisers can cooperate effectively in terms of Migrant Investor Category.

When providing immigration services regarding Investor Visas of New Zealand, a Licensed Immigration Adviser (LIA) often needs to work effectively with Financial Advisers and these professionals should clearly define their job responsibilities to ensure the client obtains a New Zealand Resident Visa through investment smoothly.

New Zealand Investor Visa is a typical time-for-space model, in which the applicant exchanges the time cost of the capital for the easy switching of identities between his residential country and New Zealand. This is because:

Firstly, although an acceptable investment requires a ‘commercial return’, term deposits are therefore not acceptable. However, Immigration New Zealand (INZ) accepts bonds as investment, such as New Zealand government bonds, which are considered to be almost risk-free fixed income investments. That is to say, to a considerable extent, it allows the investment to be ‘capital protected’. The applicant can invest only the time value of his nominated funds in exchange for little risk of the loss of principal.

Secondly, the New Zealand Permanent Resident Visa (PRV), which will be available at the end of the investment period, is also considered the only real PRV in developed countries worldwide. Once the applicant obtains it, he does not need to change his nationality, and he can freely travel in and out of New Zealand at any time without any requirement in terms of time spending there. This is particularly in the favour of Chinese applicants as China only recognises one nationality. With this PRV, Chinese Investor Migrate clients do not need to give up their passports while still enjoying the freedom of travelling to New Zealand. In another similar migrate destination, Australia, the PRV usually only has a 5-year travel facility.

Therefore, the investment is a bridge, a pathway, and the Resident Visa / Permanent Resident Visa is the goal. Naturally, the structure of the bridge (the range of acceptable investments) varies depending on where the funds are physically located (local foreign exchange regulatory requirements).

Generally speaking, if the nominated funds are in mainland China, the most secure investment channel is to purchase financial products named Qualified Domestic Institutional Investor (QDII) funds from specific banks or financial institutions approved by INZ.

Meanwhile, if the funds are in countries and territories which do not have foreign exchange controls, the range of investments accepted by Immigration New Zealand is much wider, from angel investments, bonds to equities, starting your own business, investing in commercial assets to residential developments.

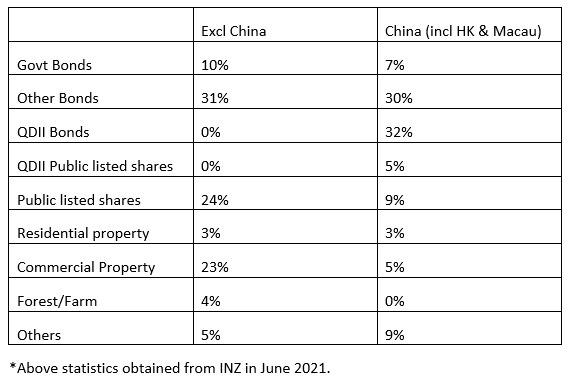

However, clients tend to choose bonds and stocks as investments due to their unfamiliarity with the business environment and regulatory frameworks in New Zealand. Meanwhile, Investor 1 and Investor 2 clients may choose a different kind of investment as the living requirements during the investment period are significantly different.

INVESTMENT MADE BY INVESTOR 1 & 2 APPROVED MAY 2017 TO SEP 2020*

At such times, typically around the stage of obtaining Approved in Principle (AIP), LIAs need to consider carefully whether they are burdened with additional regulatory controls in the course of their practice: providing financial advice. Someone giving financial advice in New Zealand is required by the Financial Advisers Act 2008 (FAA) to hold a relevant licence.

Meanwhile, the Act also defines exemptions, and exemptions to reflect the objective existence and to balance the operability. The exclusions, in the Section 10(3) of the FAA are:

- Providing information (e.g., the cost or terms and conditions of a financial product);

- And after treatment by priests or giving an opinion relating to a class of financial products (e.g. A group of financial products with similar characteristics);

- Priests or giving an opinion about the procedure for disposing of a financial product;

- The financial advice of another (unless A gives A’s own financial advice in doing so or holds out the Anxious financial advice as A’s own financial advice); or

- And after that a person consulted a financial adviser.

The exemptions in relation to LIAs are in the Section 13(1) of the FAA, which is set as incidental service:

‘A service is not A financial adviser service for the purposes of the Act if the service is provided only as an adviser incidental part of another business that is not otherwise a financial service or does not have, As its principal activity, the provision of another financial service.’

We believe that, in the general sense, LIAs in the operations of investment immigration business, are not regulated by the FAA. That is to say, the vast majority of the advice is under Exclusions or Exemptions above.

For example, recommending the client consider buying QDII products to meet the investment requirements, is excluded under section 10(3) FAA. Another example is, during the assessment of INZ, a client asks about the length of it in order to invest immediately after receiving AIP, and the LIA suggests a specific financial product which can be withdrawal every day. This is exempted under Section 13(1) of the FAA.

However, LIAs should still consider whether they have the relevant business capability firstly, as this is required under 8A of their Code of Conduct, working within the scope of your knowledge and skills.

We suggest that, in the process of application, if necessary and with the consent of the client, reliable Financial Advisers should be introduced as soon as possible. This will not only protect LIAs ourselves, for example, there will be no unnecessary compliance requirement in terms of providing financial advice, but also provides methods of risk prevention and controls for the clients in terms of their investment. We also encourage LIAs to seek independent legal advice to examine their specific circumstances in detail.

Finally, we could give the final suggestion to our LIAs that getting written consent of your clients before disclosing any personal information to third parties even if they have already engaged with that third party. Again, that’s your responsibility under 4A of their Code of Conduct.

Before migrating to New Zealand, Jessica has worked in the head office of Agricultural Bank of China for 14 years, dealing with non-performing loans. She has a lawyer qualification of China and she is also an Arbitrator of Xiamen Arbitration Commission currently.

IMME Limited has been established by Jessica, focusing on New Zealand Investor Category visas. Serving clients include the founder families of companies listed in Major Global Stock Markets, such as Nasdaq in the United States, A-share market in Mainland China and ASX share market in Australia. Contact Jessica at imme@immegrationz.com